BARCLAYS (BCS)·Q4 2025 Earnings Summary

Barclays Delivers 11.3% ROTE, Raises 2026 Guidance to £31B — Stock Jumps 3%

February 10, 2026 · by Fintool AI Agent

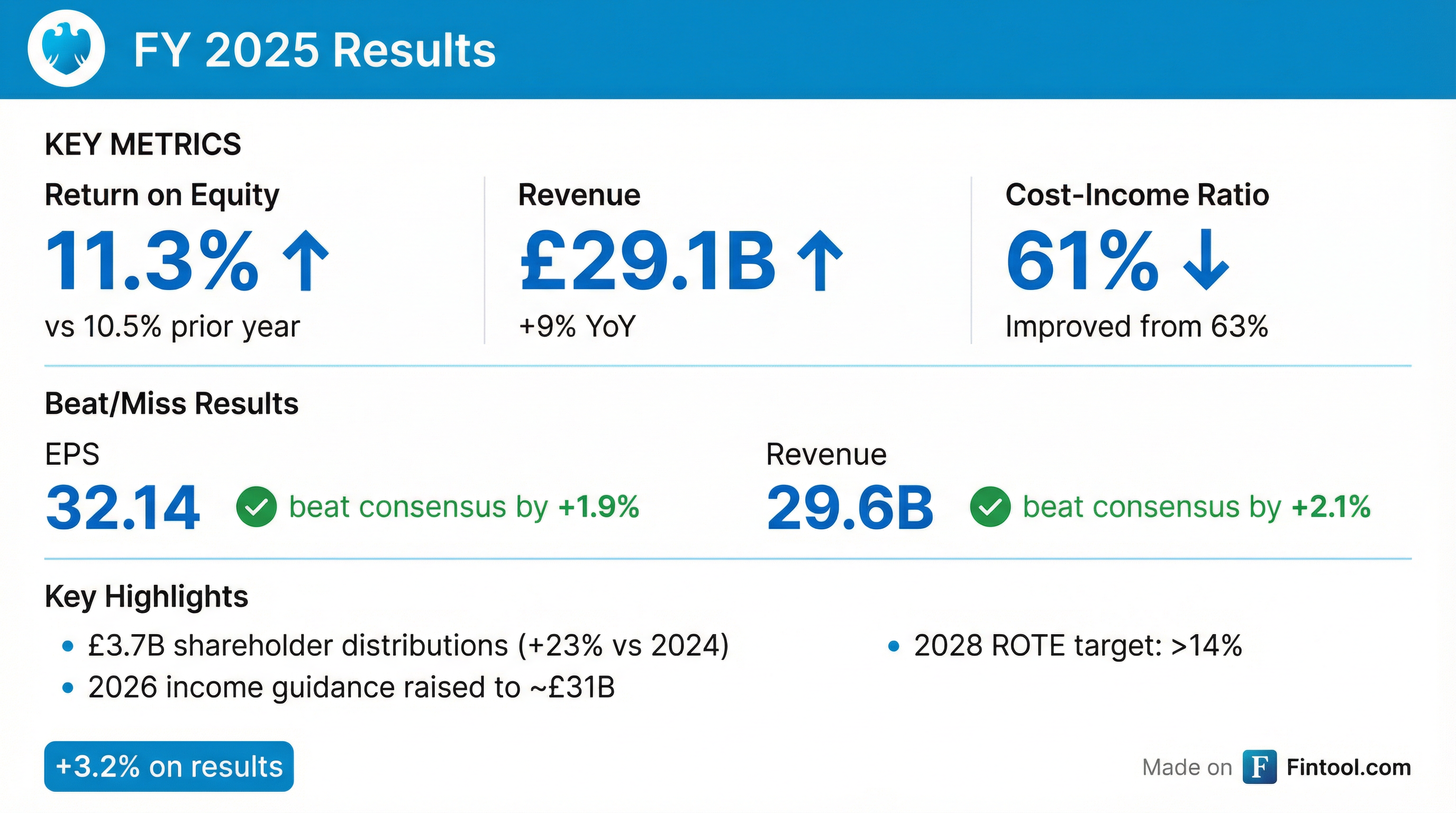

Barclays reported Q4 2025 results that beat on both earnings and revenue, delivering a full-year return on tangible equity of 11.3% and raising 2026 income guidance by £1 billion to ~£31B. CEO Venkat outlined an "accelerating ambition" phase targeting >14% ROTE by 2028 with >£15B in shareholder distributions. The stock jumped 3.2% on the results.

Did Barclays Beat Earnings?

Yes — Barclays beat on both EPS and revenue.

For the full year 2025, Barclays achieved all financial targets:

CEO Venkat highlighted the strategic progress: "We are moving from a period of measured ambition to one of accelerating ambition. We aim for sustainably stronger returns, greater shareholder distributions, and operational excellence."

What Did Management Guide?

Barclays raised 2026 guidance and introduced new 2028 targets.

2026 Outlook

CFO Anna Cross noted: "The strength and predictability of this growth means we are upgrading our expected group income to circa £31 billion in 2026 versus circa £30 billion previously."

New 2028 Targets

The 2028 ROTE target of >14% compares to 11.3% achieved in 2025 — a significant step-up requiring continued operational improvement.

What's Driving the Improvement?

Structural Hedge Tailwind

The structural hedge is a major income driver, now contributing 46% of group NII (excluding IB and head office).

Management extended the average hedge duration from 3 to 3.5 years, which "reduces the quantum of maturing hedges to circa £35 billion per year from around £50 billion in recent years. This slows the pace of structural hedge income growth, but therefore prolongs the expected positive effect until at least 2029."

UK Business Momentum

All three UK divisions delivered double-digit ROTE:

UK lending grew 4% YoY with strong mortgage and credit card momentum:

- Mortgage applications at highest level ever

- 1.4M new credit card customers (up from 1.1M in 2024)

- UK corporate bank lending +18% YoY

- Market share in corporate banking +100bps to 9.6%

Investment Bank Progress

The Investment Bank delivered 10.6% ROTE in 2025, up 210 basis points from 8.5% in 2024.

The 2028 target for IB ROTE is >13% with income-to-RWAs >7%.

Capital Return Story

Barclays announced £3.7B in distributions for 2025, up 23% from £3B in 2024:

The bank ended 2025 with a CET1 ratio of 14.3% — at the top of the 13-14% target range.

Going forward, Barclays is evolving its distribution mix:

- Dividend increase to £2B in 2026 (from £1.2B)

- Move to quarterly buybacks (announced Q3 2025)

- Total distributions 2026-28: >£15B

CFO Anna Cross emphasized: "Given this strong capital position, we have announced a £1 billion share buyback and a £0.8 billion final dividend equivalent to 5.6 pence per share."

How Did the Stock React?

BCS shares rose 3.2% following the earnings release, closing at $26.71.

The stock has nearly doubled over the past year as Barclays delivered on its turnaround plan and returned substantial capital to shareholders.

What's New This Quarter?

Best Egg Acquisition

Barclays announced plans to acquire Best Egg, a digital lending platform, in Q2 2026.

"The acquisition of Best Egg in the second quarter of 2026 will further expand the breadth of our digital capabilities. Around 90% of Best Egg's consumer loan originations come through digital channels."

Expected Best Egg impact:

- Operating costs: ~£0.3B in 2026, ~£0.4B in 2028

- Will be integrated with US card partners for cross-selling

- Supports ABS origination in the Investment Bank

AI and Technology Transformation

Barclays is doubling technology investment through 2028, with a major AI focus:

CEO Venkat emphasized: "For some time now, technology has revolved around our businesses. Now, our businesses are revolving around technology."

US Consumer Bank Evolution

The US Consumer Bank delivered 11% ROTE in 2025 (up from 9.1% in 2024), with several moving parts in 2026:

The American Airlines portfolio sale in Q2 2026 will remove a low-margin, superprime book, improving overall NIM.

Digital Assets and Tokenization

Barclays is positioning itself as a leader in digital asset innovation, with several initiatives underway:

Group Treasurer Dan Fairclough noted: "Digital assets present the opportunity to significantly transform key activities within the financial services industry for our clients, and we are excited to drive this transformation."

The GBTD pilot will test both retail use cases (remortgages) and wholesale use cases (corporate bond issuance and investment).

Capital Structure and Funding

The fixed income investor call provided additional detail on Barclays' capital and liquidity position:

2026 Funding Plan

Barclays expects to issue £10B of MREL in 2026, down from £16B in 2025, with a skew towards senior debt:

- No AT1 calls in 2026

- Limited AT1 and Tier 2 issuance expected

- Extended weighted average life at historically tight spreads

- Currency diversification including non-call 10 euro AT1 and non-call 20 senior

Regulatory RWA Inflation Timeline

Following these changes, Barclays expects a reduction in Group Pillar 2A requirement.

Credit Rating Ambitions

Barclays targets single A composite rating at the PLC senior level, which would require an upgrade from either Moody's or S&P. Management believes the 2028 targets — increased profitability, greater capital generation, and group rebalancing — support this objective.

Q&A Highlights

On Capital Capacity

When asked about the >£15B distribution target relative to capital generation, CFO Anna Cross clarified there's deliberate excess capacity built in:

"The level of generation actually surpasses both of those two increases [distributions and investment]. So what we've done here is we've deliberately created some capacity for us to be able to invest further if and only if we determine that is the right thing to do... We have no inclination, no objective here to hold on to higher than required levels of capital."

On Investment Bank RWA Discipline

The IB will remain at ~50% of group RWAs through 2028:

"We don't have an explicit target in terms of number of employees. What I've said is there will be productivity benefits from all these investments... It's no accident that the most digitally enabled part of the bank, which is the U.S. Consumer Bank, also has our lowest cost-income ratio."

On Inorganic Growth Criteria

CFO Anna Cross outlined the three-part framework for evaluating acquisitions (referencing Kensington, Tesco, and Best Egg deals):

- Strategic Fit: Must clearly further the strategy — delivering volume or capability

- Price: Absolute ROTE/ROIC, EPS accretion, and return vs. a buyback

- Integration Simplicity: Avoid complicated integrations that distract from executing the plan

"If we haven't [done deals], it's because one of those boxes remains unticked."

On why Barclays operates at the top of the CET1 range: "Until we have that regulatory clarity and the NDA drops again, then you should expect to see us towards the top end. So that's why we're operating at that end rather than any expectation that you should link that to an inorganic move."

On Synthetic Risk Transfer (SRT) Strategy

Barclays' SRT program totals £54B of notional exposure, with the Colonnade program at scale:

- Colonnade: Mature, broadly at scale — focused on RWA amortization management

- UK Business: Targeted transactions in mortgages and consumer loans (including first UK consumer loan securitization in Q4)

- Best Egg: Originate-to-distribute model, relatively modest activity expected

"We really do think about SRT as a risk management tool... the hedge ratios that we want to run across the portfolio is a key factor."

On Mortgage Margin Headwinds

CFO Cross flagged a temporary headwind in H1 2026 from stamp duty holiday mortgages refinancing:

"Those mortgages were written at very widespread, like 160 basis points. That's quite meaningfully different from where we are now. So just as they refinance, you're going to see some relatively short-term pressure... We think it'll be gone by the end of half one."

Key Risks and Concerns

-

Regulatory RWA Inflation: £19-26B of regulatory RWA headwinds expected, including ~£16B from IRB migration in US consumer bank

-

UK Motor Finance Provision: £235M provision taken in Q3 2025 for potential motor finance remediation — without this, cost-income ratio would have been 60%

-

Investment Bank Fee Share: Despite investments in bankers, fee market share gains have been slower than expected in ECM and M&A

-

US Consumer Bank Complexity: Multiple moving parts (AA sale, GM portfolio migration, Best Egg acquisition) create execution risk in 2026

Forward Catalysts

Bottom Line

Barclays delivered a clean beat on Q4 2025 results and hit all full-year targets, validating the turnaround strategy launched in February 2024. The raised 2026 guidance (+£1B income) and new 2028 targets (>14% ROTE, >£15B distributions) signal management confidence in sustained improvement. Key drivers include the structural hedge tailwind, UK business momentum, and continued Investment Bank productivity gains.

The stock's +86% run over the past year reflects investor recognition of the transformation, but 2026 execution carries meaningful complexity — particularly the US consumer bank portfolio changes and Best Egg integration. The >14% ROTE target for 2028 remains ambitious and will require continued cost discipline alongside revenue growth.

Data sources: Barclays Q4 2025 earnings call transcript , Barclays Q4 2025 fixed income investor call , S&P Global